By

·

5 minute read

By

·

5 minute read

BLUF: The war in Iran has once again highlighted critical vulnerabilities in the international rare gas trade, where geographic concentration of suppliers can lead to oversized risks and disruptions, though Northeast Asian consumers are taking steps to at least partially mitigate the risk of short supply chain disruptions.

Analysis: The war in Iran has disrupted the flow of crude oil and natural gas from the Middle East, raising global prices. The immediate second-order impacts include supply chain stresses to refined fuels (heavy fuel oil, diesel, automotive gas, and aviation fuel), fertilizer production, and the chemicals industry. But the conflict is also impacting the availability of rare gases, particularly Helium, which is critical to the semiconductor industry, among others. Helium is used in Extreme Ultraviolet lithography (EUV), as a coolant for semiconductor materials, and as a carrier gas, and helps ensure a clean environment allowing higher tolerances in the manufacturing process.

Prior to the conflict, Qatar supplied just over a third of global helium, with the United States producing just over 43 percent. However, Iranian strikes near Qatar’s helium processing facilities triggered Doha to trim production. Qatar’s helium comes from wells in the North Field, which primarily produces natural gas (helium composition in the field is just 0.04% of the total gas reservoir, a fairly low percentage), and is processed at the Ras Laffan helium plants north of Doha on the Persian Gulf. Qatar’s North Field contains an estimated 10.1 billion cubic meters of helium, according to the US Geological Survey (USGS), about a third of total U.S. reserves, but higher than any other country. Qatar’s Helium 1 plant began operations in 2005, its Helium 2 plant in 2013, and the small country quickly became a major supplier of helium to the global market for medical and industrial uses, including in the semiconductor industry.

In addition to its larger production, the United States formerly held a strategic reserve of helium underground in old natural gas fields, but in 2004 the Bureau of Land Management (BLM) completed the sale of the national stockpile to the New Jersey-based Messer Americas, a part of Germany’s Messer Group. Although semiconductor manufacturers do try to maintain several months of stockpiled helium (South Korean companies have reported holding six-months of supplies), the tiny size of the helium molecule does lead to slow losses, limiting extremely long-term storage. Many Asian semiconductor companies have also stepped up helium recycling at their facilities (along with other rare gas recovery and recycling) to buffer against supply shocks.

While the war in Iran is triggering supply side shocks to the global helium market, the war in Ukraine had already highlighted risks to other critical rare gases used in the semiconductor industry, most notably Neon. Neon is the key carrier gas (along with Argon or Krypton) in deep ultraviolet (DUV) lasers, used for etching the patterns on semiconductors. Although relatively ubiquitous (as opposed to the geographic concentration of helium supplies), neon makes up 0.0018 percent of the atmosphere, requiring significant cooling and distillation processes to capture and purify from the air. This is primarily done via very large Air Separation Units (ASU), which are most often associated with older types of steel mills. The capture of neon is a secondary process - the primary purpose of the ASUs is to produce high-concentration oxygen from the atmosphere to improve the efficiency of the steel blast furnaces. While Oxygen, Nitrogen, and even Argon are typically captured products from ASUs, other gases (including neon, krypton, and xenon) require additional steps due to their extremely low atmospheric concentrations, and most steel plant ASUs are not designed to capture these affiliated gases.

Soviet-era steel plants, however, were designed to be both very large, and to capture additional gases from their ASUs, largely as part of the Soviet Union’s attempts to ensure national industrial self-sufficiency. The legacy plants in Ukraine became key suppliers of neon, as well as krypton and xenon, for global semiconductor manufacturers. The 2014 Russian annexation of Crimea disrupted rare gas supplies from Ukraine, and the 2022 invasion of Ukraine further threatened Ukraine’s reliability as a key supplier of rare gases. South Korea and Japan have both moved to decrease reliance on imported neon, xenon, and krypton (as well as helium as noted above), investing in updated ASUs to produce rare gases at home, and in capture and recycling of key gases to reduce dependence on new imports. Between 2014 and 2022, Ukraine saw its share of global neon supplies to the semiconductor industry fall from 70 percent to around 50 percent, largely due to the actions of the Asians and to the continued degradation of domestic capacity due to war.

There are other critical gases to the semiconductor industry that have constrained supply chains, including Tungsten Hexafluoride, Nitrogen Trifluoride, Chlorine Trifluoride, and Silane Gas, among others. Like the Rare Earth Metals and critical minerals, rare and critical gases are often either constrained in limited reserve locations, or face high concentrations of production within a single country or region. Geopolitical disruptions, from war to political change to international disputes, can quickly lead to limited or large-scale supply chain disruptions, at times aimed at single recipients (South Korea and Japan have had several spats that limited gas transfers between the countries, Japan and China have seen unofficial constraints on transfers of critical minerals). The triple hit of the Ukraine war, Iran war, and U.S.-China trade war show the fragility of the global supply chains of critical gases, and are starting to drive technological and process responses, each of which has a financial and time cost associated.

A challenge in monitoring vulnerabilities in rare gas supply chains comes in part from limits of reporting - many of these gases are seen as issues of national economic security, or are filed only under broad categories (HS 280429 covers all rare gases aside from Argon, and thus includes neon, xenon, krypton, and others, without differentiating). The World Bank’s World Integrated Trade Solution (WITS), for example, shows rare gas exports from Qatar to other countries in their import statistics, but records no exports of rare gases FROM Qatar, making it complicated to piece together the whole of the country’s exports compared to other suppliers.

National-level trade statistics also rarely differentiate the purity of gasses (in the semiconductor industry, gasses often need to be at a 5n or 6n level of purity, meaning 99.999% or 99.9999% pure, removing any trace metals or moisture, even before dopants are added (additional gases or metals in very small concentrations), meaning crude gases may be exported either for less technical uses, or for refinement further in the importing country.

The four charts below, however, do offer some insight into the ways different countries manage the global rare gas supply chain, and the role Qatar has played in recent years.

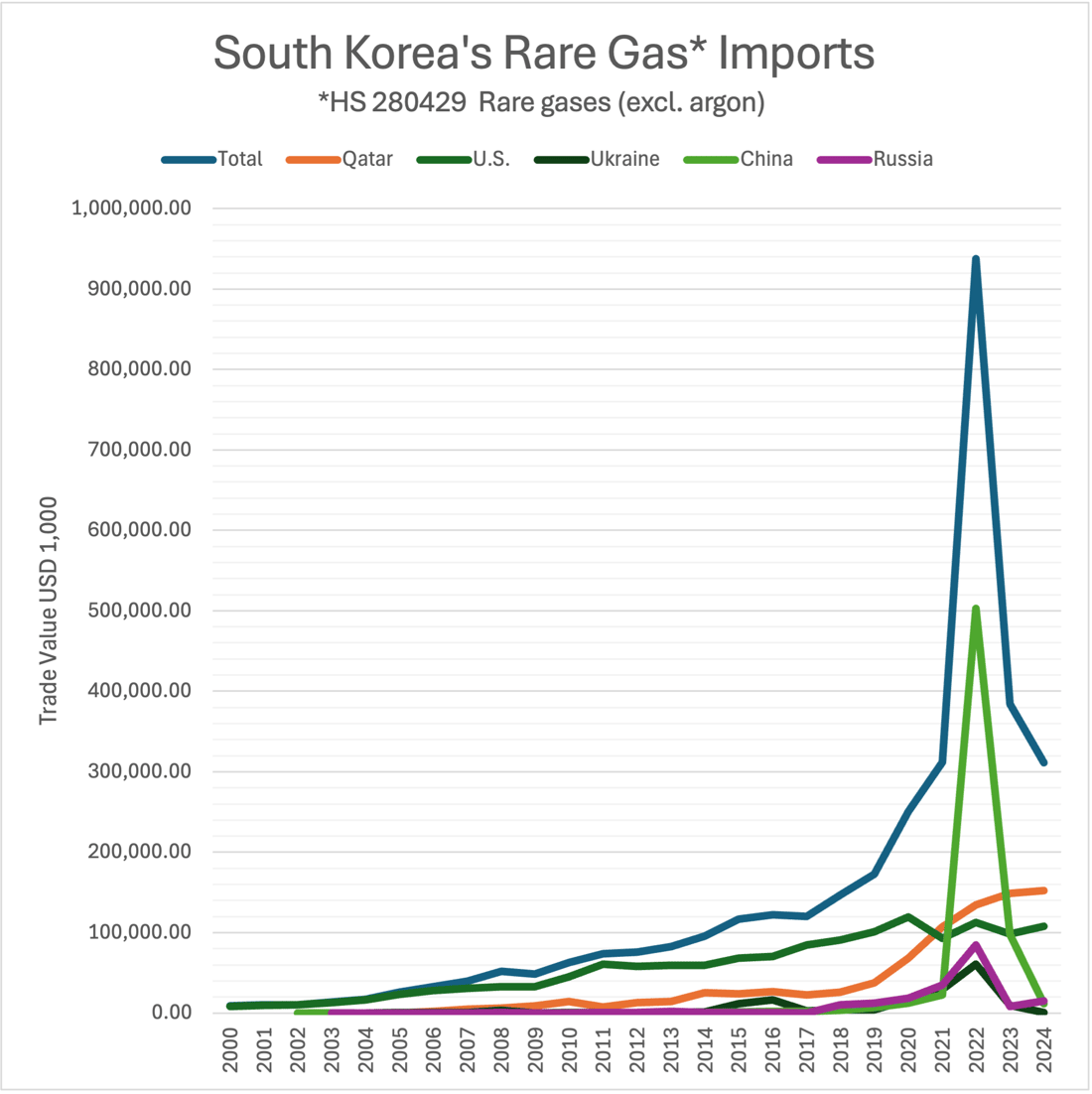

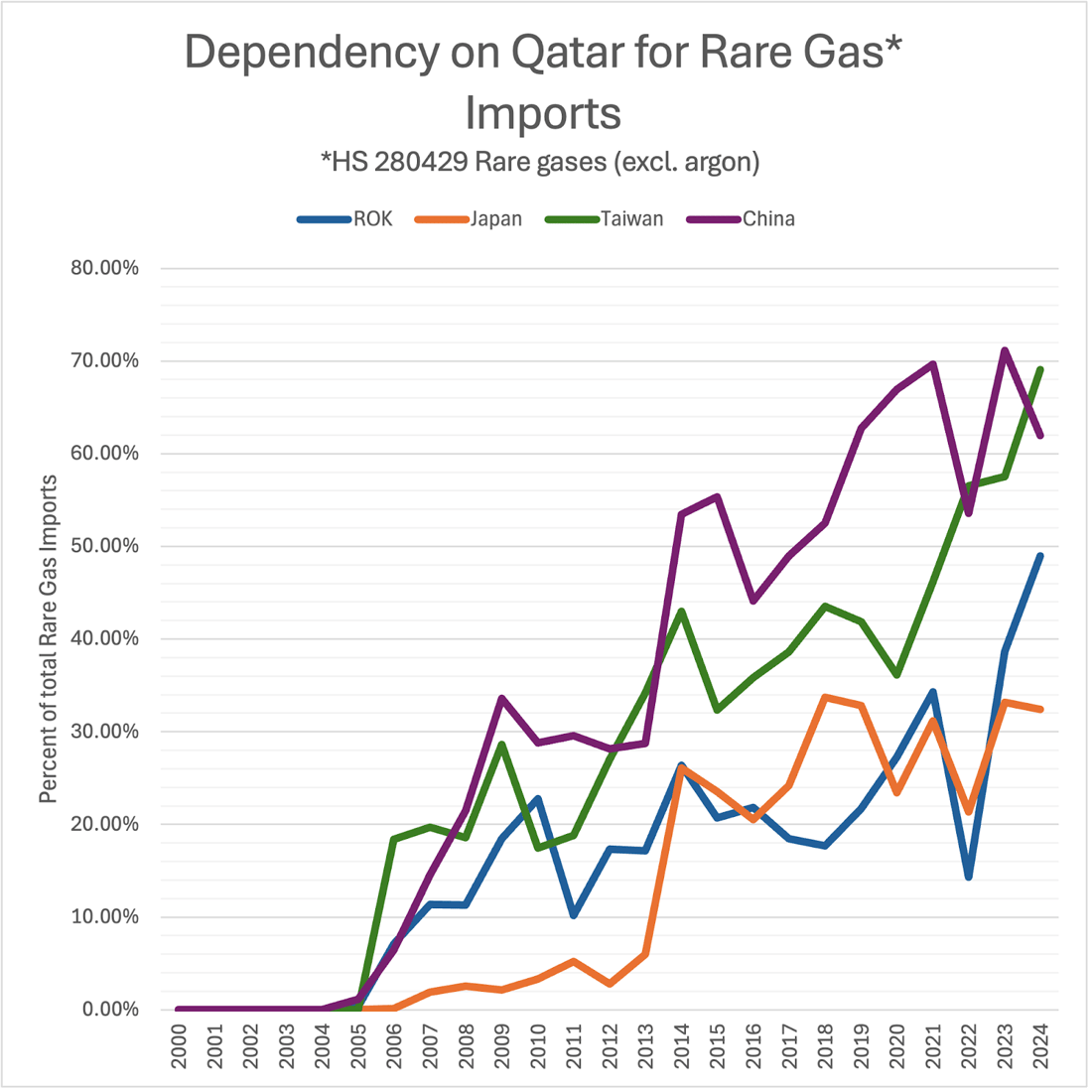

The entrance of Qatar into the global rare gas supply market allowed South Korea to start to reduce its heavy dependence on the United States by around 2020. South Korea’s response to the 2022 Russian invasion of Ukraine was a massive surge in imports to stockpile - an oversized reaction triggered by South Korea’s challenges faced in the 2014 Russian annexation of Crimea and in their 2019 spat with Japan, where Tokyo limited critical gas exports to South Korea. South Korea has also undertaken significant investment in the domestic production of rare gases, and in the capture and recycling of gasses at semiconductor facilities.

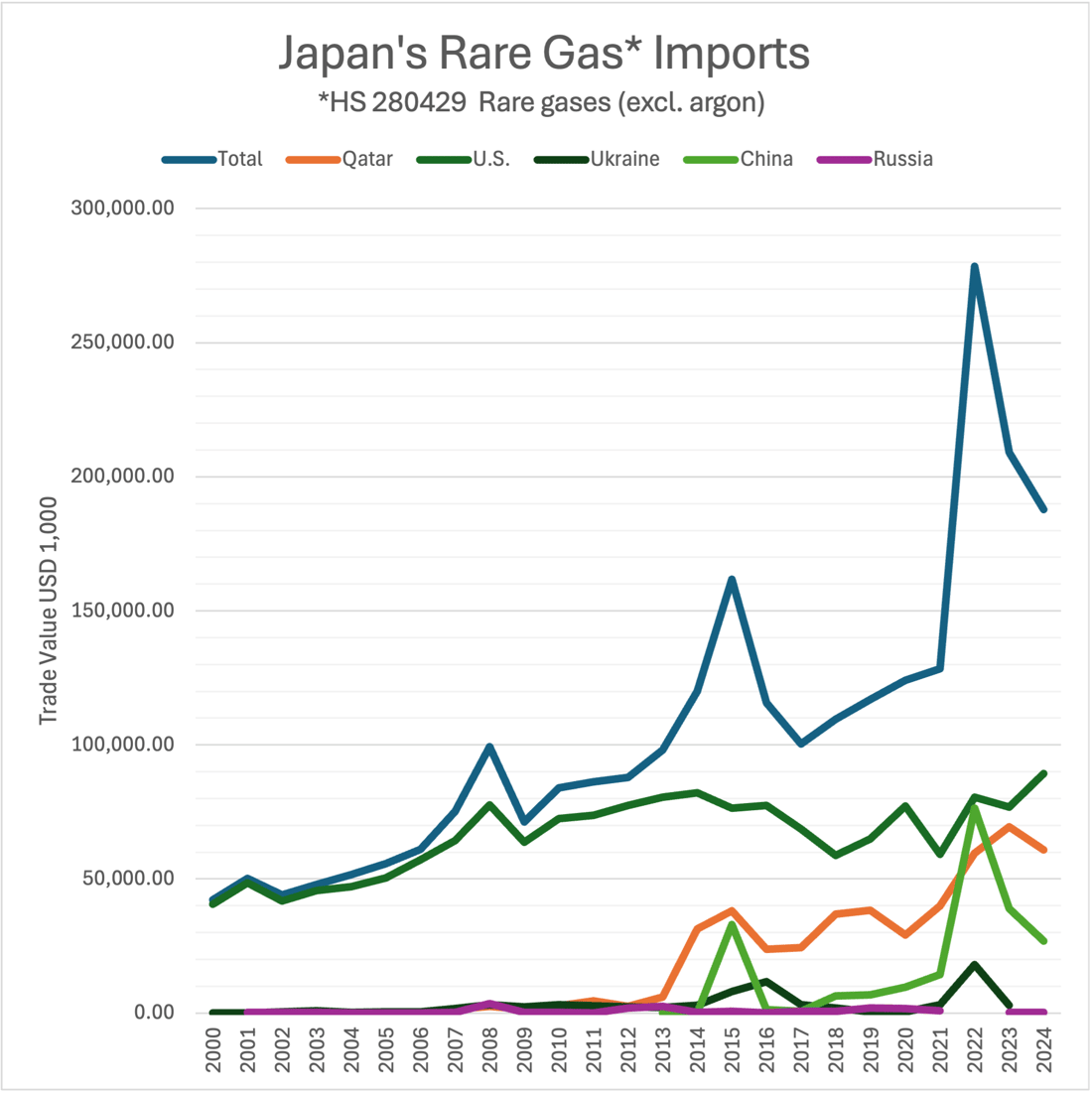

Japan moved even faster than South Korea in breaking its over dependence on the United States for rare gases, with the shift coming by 2014-15. Like Seoul, Japan surged imports of rare gases in 2022, but not nearly to the levels seen in South Korea. While not shown on the graph, Japan has long had a more diverse set of suppliers for its rare gases than South Korea, perhaps allowing it to better weather short regionally-isolated supply chain disruptions.

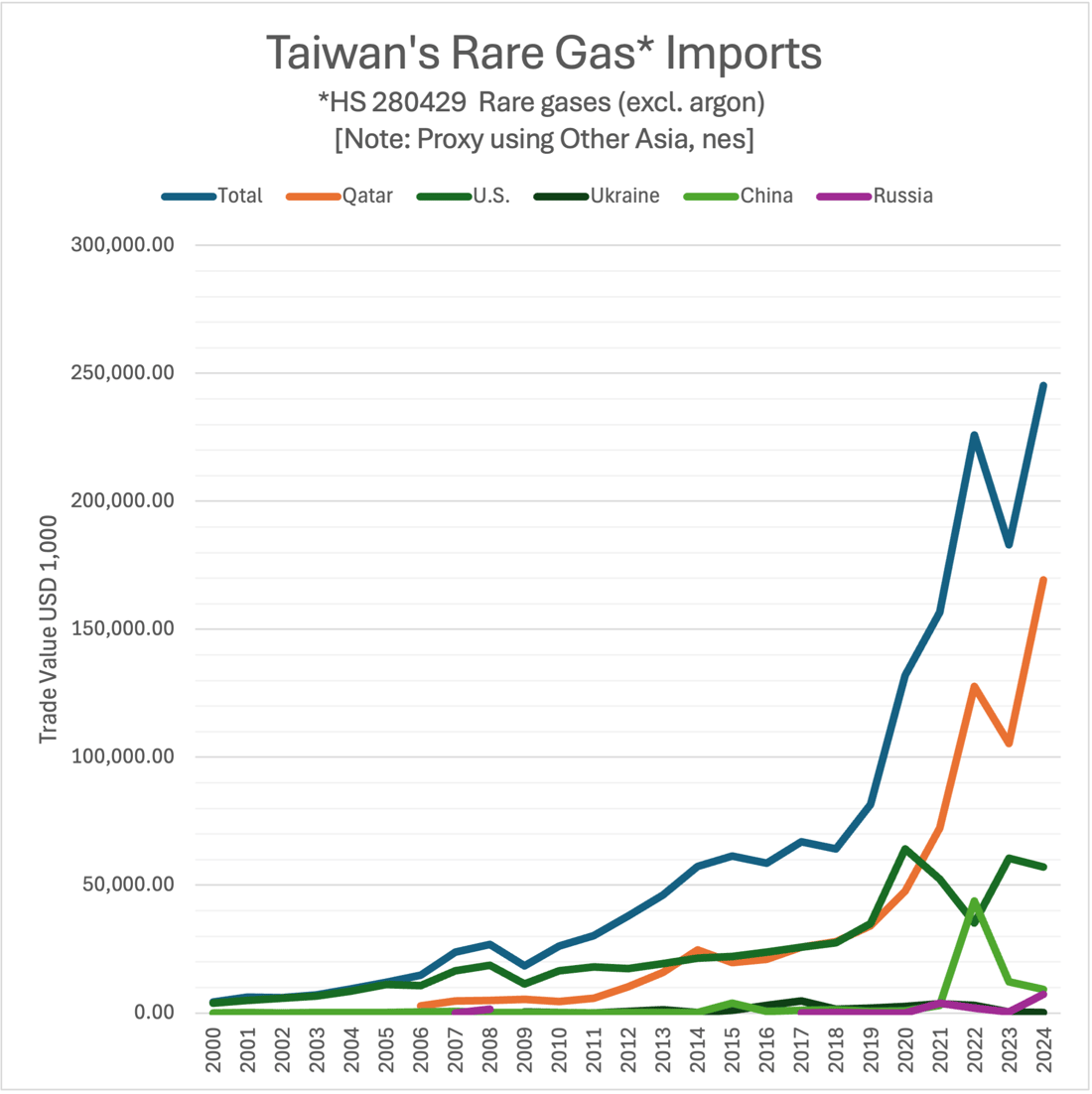

Taiwan is slightly harder to suss out, as it is not formally included in WITS data (but rather falls under the euphemistic category “Other Asia - nes (not elsewhere seen).” Taiwan’s dependency on Qatar for rare gases rises dramatically, with Qatar supplying just over 69 percent of Taiwan’s total imports of rare gases in 2024, compared to Japan’s 32 percent and South Korea’s 49 percent dependency, suggesting Taiwan is the most exposed of the northeast Asian countries currently, Japan the least.

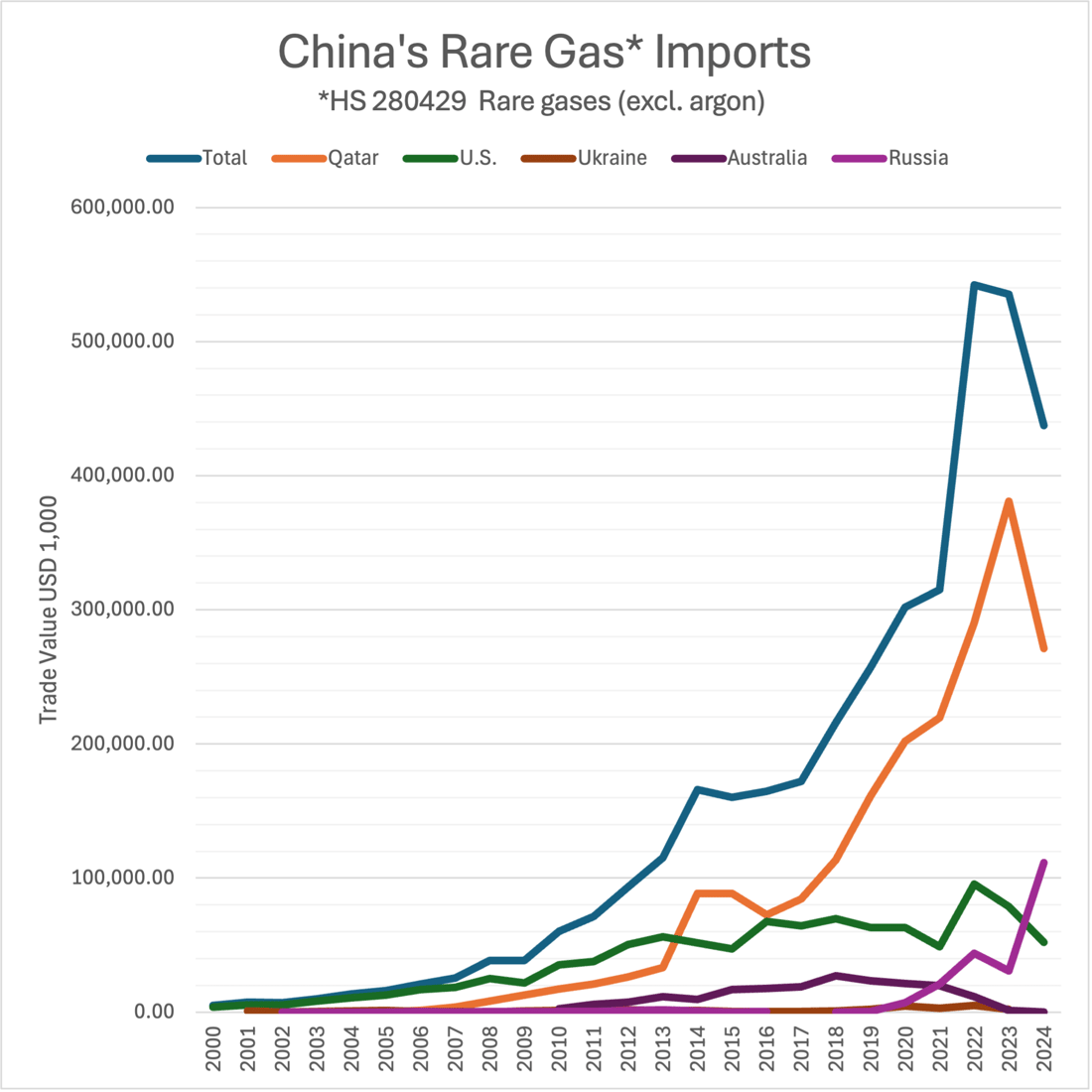

Finally, we see China, which like Taiwan has become heavily dependent upon Qatar (reaching more than 71 percent of imports in 2023, falling slightly to 64 percent in 2024). Like Japan, China’s overall mix of suppliers is fairly widespread, but it remains most dependent on Qatar and the United States (until its recent surge of purchases from Russia). That all four of the Northeast Asian are dependent upon the same basic set of suppliers highlights the fragility of supply chains of rare gases. At the same time, in each of the countries, to differing degrees, we are seeing a surge in investments to enhance domestic production, innovate to conserve and recycle critical gases, and develop at least company-level reserve stockpiles to ease short-term supply chain disruptions.