By

·

5 minute read

By

·

5 minute read

BLUF: Nearshoring in Mexico rests on USMCA renegotiations and the US-global tariff gap. Rather than a question of labor arbitrage, the relative balance of cost between the Mexico-US tariff rate for finished products and the sum of input tariff rates for U.S. produced products will strongly influence investment decisions. We expect anti-China concerns from Washington to shape the USMCA renegotiation cycle, but over time Mexico will likely remain a primary near-shoring location due to entrenched infrastructure and relations.

Key Points

- USMCA negotiations will be slow, but will eventually renew with a greater focus on limiting Chinese throughputs.

- Input cost arbitrage, not labor, now drives Mexico’s nearshoring decision calculations

- Nearshoring has slowed in recent months, but has not reversed

- China’s actual footprint in Mexico is modest, and Beijing is likely to continue to tread cautiously that close to the United States.

- Kinetic anti-cartel policies are the dominant tail risk to an otherwise stable base case

Even with negotiations slow and contentious, the question isn’t whether the USMCA survives, but how its rules of origin, content thresholds, and security overlays are redrawn. The likely result is a tighter, more anti-China agreement that leaves Mexico the default friend-shoring platform, even if some aspects of U.S. trade policy seek to increase onshoring, rather than preference near- or friend- shoring. Although China has gained ground in exports to Mexico (many of which flow-through to the United States), we do not expect the current political and economic friction between Washington and Mexico City to open a significant space for Beijing to exploit - even if they wanted to. In short, Mexico’s nearshoring advantage is real, based on long-standing structural dynamics (infrastructure, existing concentrations of activity, etc), but it is also based on shifting conditions, particularly the relative balance of tariffs.

The USMCA talks are a renegotiation in all but name, with USTR Jamieson Greer has said that a rubberstamp is not in U.S. interests. Each side has brought different suggestions on what they want to to extend the agreement for another six years (or more, in Canada’s case). Failing to agree by the July 1 deadline shifts the requirement for discussion and review from a six-year cycle to a 1-year cycle, increasing uncertainty for companies seeking long-term predictability in the agreement. Should the parties fail over the next 10 years to agree on a long-term extension, the deal could expire in 2036. The core U.S. administration intent (at least publicly) is to convert the USMCA into a counter-China economic security instrument. To do this, Washington is pursuing tighter rules of origin (vehicles first, pushing for 50% U.S. content, followed by electronics, aerospace, medical devices, etc.), greater oversight of Chinese FDI, and transshipment traceability.

Looking forward, we see four plausible pathways for the USMCA dynamics to evolve over the next five years (beyond the current administration), listed in order of current likelihood.

-

USMCA extends after several months of short-term uncertainty, with tighter origin rules and China-screens; U.S.-China select decoupling persists. Mexico continues to consolidate as a prime nearshoring location. The overall balance between broader U.S. tariffs for materials and the border tariffs with Mexico shape the decisions of companies as they look at their Americas manufacturing.

-

Transactional turbulence results in no clean deal; serial reviews, parallel bilateral tracks, recurring tariff spats. USMCA survives with an uncertainty discount; investment continues to lean “defensive.” Cyclical adjustments dominate forward-looking investment, resulting in short-term horizons for businesses.

-

Security escalation/kinetic intervention leads to further U.S. strikes on cartels, crossing sovereignty red lines. Bilateral trust suffers; cartels may shift to targeting U.S.-backed industry and cross-border transportation routes.

-

Unlikely, but potential U.S.-China detente hardens into a durable trade deal; tariff gap narrows and Mexico’s arbitrage reduces. Primarily logistics and nearshoring, not focused on tariff arbitrage.

For businesses, the labor arbitrage in U.S.-Mexico trade has become less significant than the impact of import tariffs; it is an assessment of the total cost due to U.S. tariffs on precursor materials for goods ultimately manufactured inside the United States (onshoring) versus the overall cost of making in Mexico and paying import tariffs on final products rather than on the numerous inputs (nearshoring). Currently some components and materials from China exported to Mexico can effectively enter the U.S. duty-free if they are integrated into products in Mexic and thus qualify under the USMCA, but more often it is about raw materials - steel, aluminum, and the like. Companies operating in Mexico can import these input materials to Mexico without the same tariff barriers they face if operating in the United States, and by significantly altering the products and adding value, they are no longer seen as being made or produced outside Mexico and the USMCA framework. The gap between the input costs and broader tariff, and the overall impact of input costs tariffs in the US, is what is driving some financial decisions regarding relocation. The United States is seeking to alter the USMCA to assess content origin, not necessarily the location of significant value add.

A second consideration is the uncertainty surrounding the purpose of U.S. tariffs, which informs how businesses interpret their longevity and application. There has been mixed signalling from the U.S. administration, and between the administration and congress, with the three predominant (and not always mutually exclusive) frameworks being:

- Encouraging onshoring to strengthen U.S. industry and reduce trade deficits

- Raising revenue through the collection of tariffs, thus allowing select tax reductions

- Strengthening U.S. national security by reducing dependency on foreign suppliers

The challenge for companies is that the first and second stated goals are nearly irreconcilable - onshoring reduces tariff revenue; encouraging the collection of tariff revenue reduces incentives to onshore. The third goal can in some ways align with either of the other two, though it brings with it a set of additional regulations that are not specifically tariff related, and can have their own economic impact.

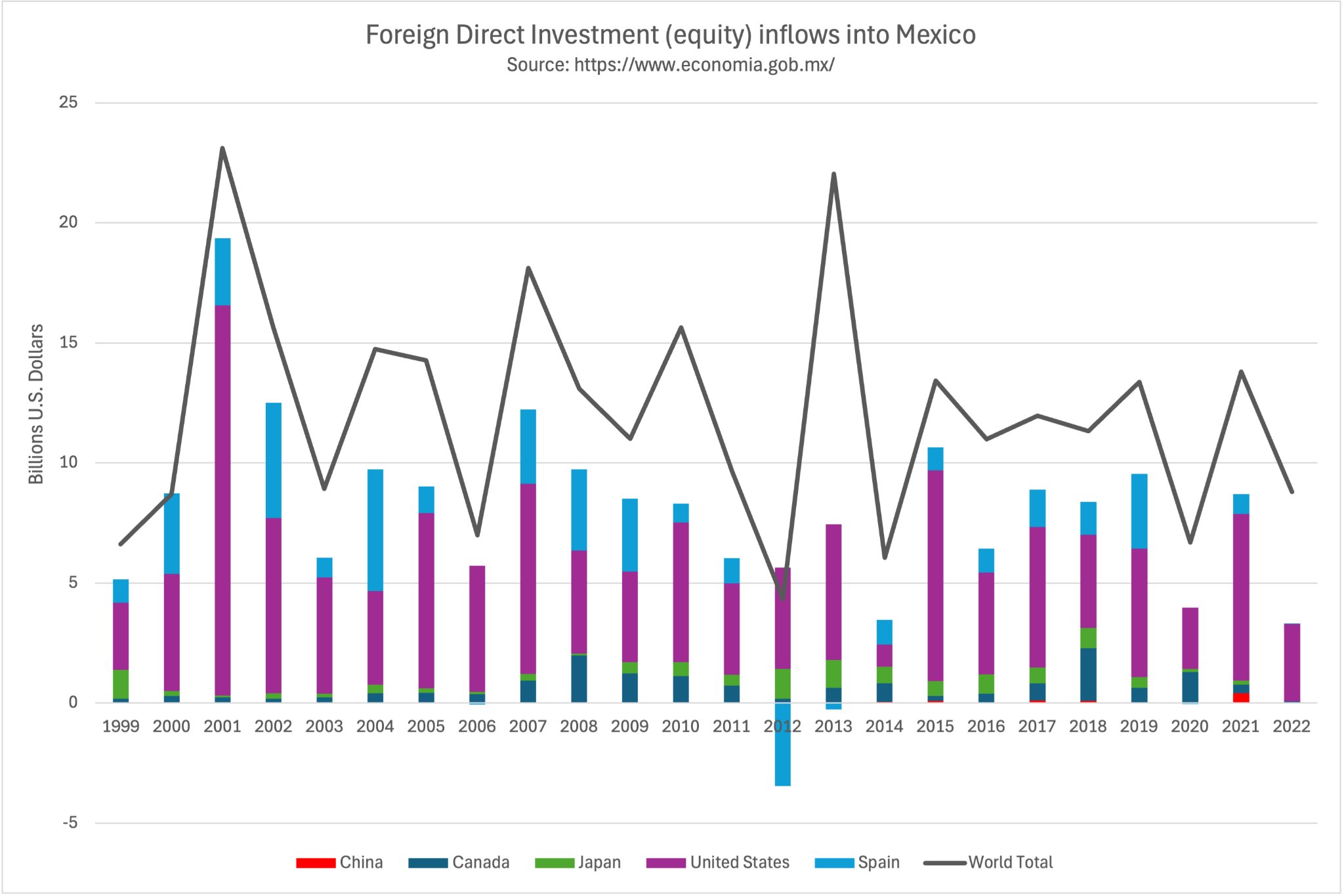

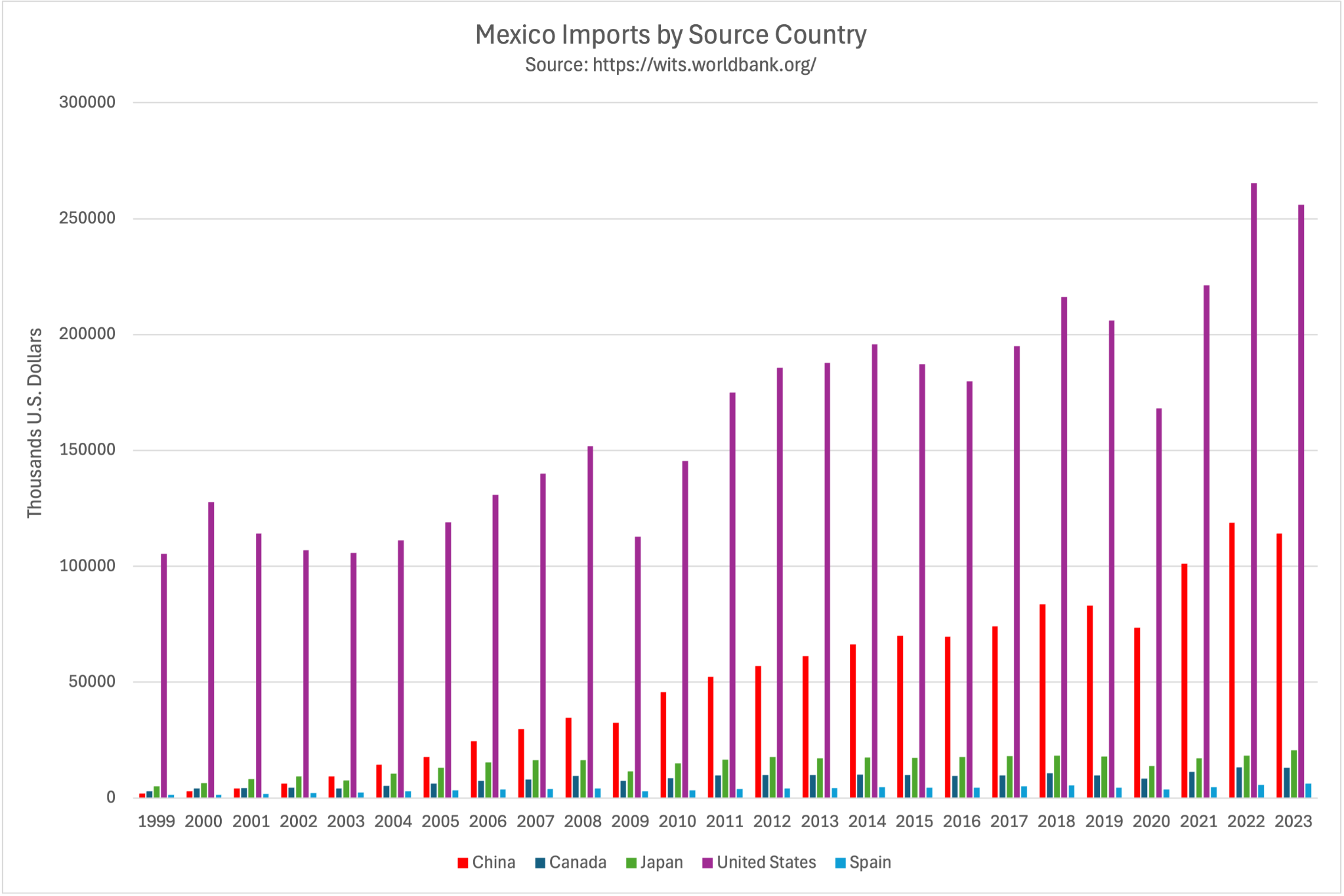

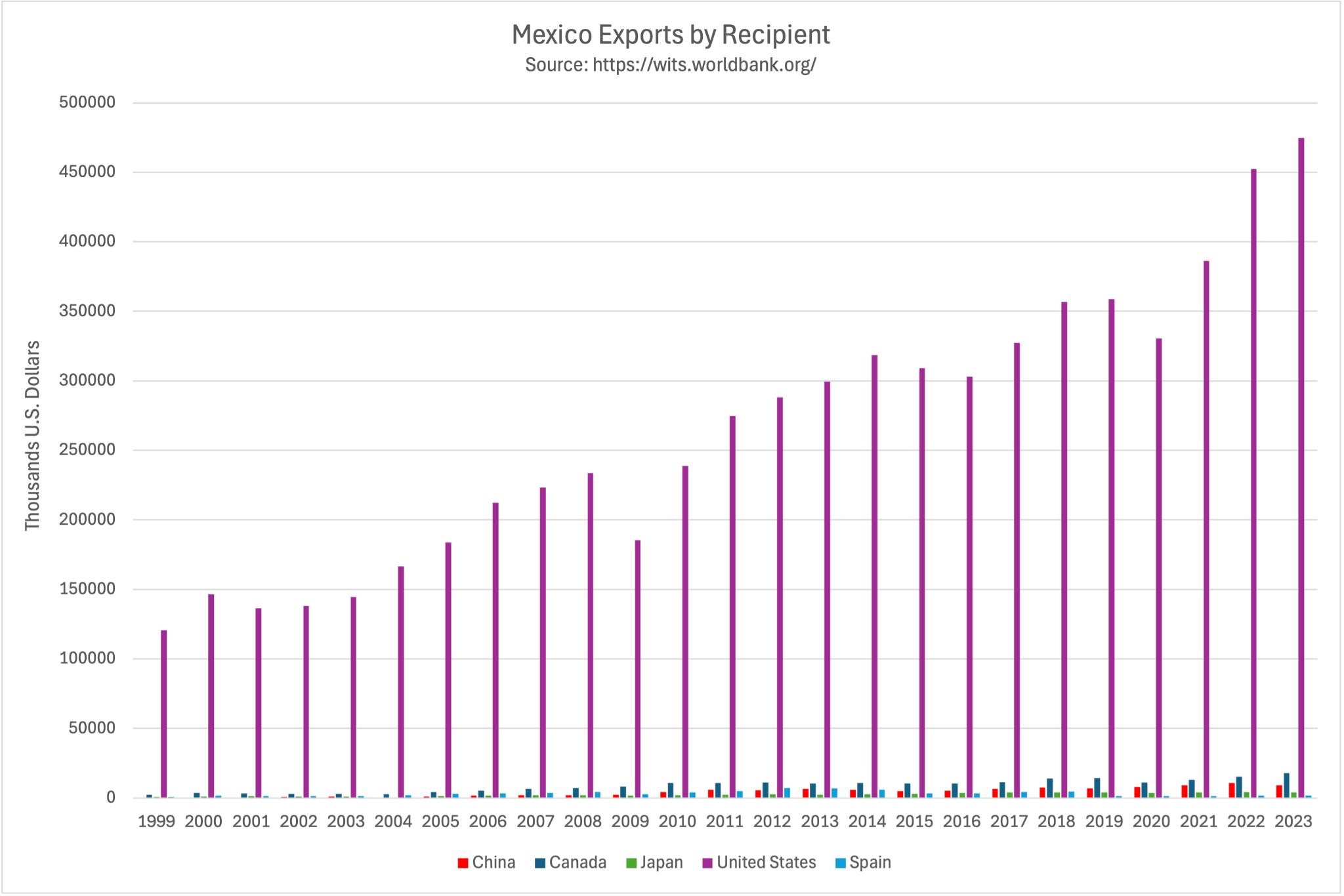

With this in mind, we can look at just how much China is engaged with the Mexican economy. China increasingly employs Mexico as a flow-through, as seen in the large increase in Chinese exports to Mexico, but the continued miniscule Chinese imports from Mexico. However, Chinese Foreign Direct Investments into Mexico remain relatively small, with even high assessments of cumulative investments from 2017-2024 lagging behind Canada, Japan, Spain, and Germany, and official numbers even lagging behind South Korea. Chinese FDI and Chinese trade with Mexico both remain far behind the United States (though Chinese exports have increased to about half of U.S. exports to Mexico annually). For now, Beijing has both limited room and limited intent to deepen its Mexican footprint beyond its use as an adjunct to U.S. trade, particularly in the automotive parts sector. At least for now, Beijing is concerned that a major surge in investment and engagement would solidify anti-China sentiment in the U.S. Congress and administration, which would further undermine efforts to ease the trade war.

As U.S. companies take stock of the USMCA negotiations and the evolution of the administration’s overall tariff policies, nearshoring trends have slowed, but not reversed. Mexico hit record inbound FDI in 2024-2025, but the composition is “defensive.” Over 80% was reinvested earnings, while new greenfield announcements fell. Nearshoring-related announcements fell nearly 78% YoY in Q1 2026. Mexico’s binding constraint is investment uncertainty coupled with energy, water, and security concerns, though the former two - water and energy - are growing concerns everywhere.

In the semiconductor and tech industry, Mexico’s primary roles are assembly, testing, packaging (ATP), and contracted manufacturing. This is supported by the CHIPS Act ITSI Fund and Mexico’s Kutsari design initiative. There has been almost zero front-end fab investment, and there likely won’t be major investment within this horizon. Workforce, energy, water, and capital are binding variables. The dominant risk is that Chinese/Asian origin content in Mexico-assembled electronics triggers new U.S. rules-of-origin or Section 232 chip tariffs.

Outside these trade concerns, a low probability high impact potential disruptor is U.S. counter-drug policies. Recent actions against El Mencho and in-country CIA activities show the U.S. willingness to press forward with kinetic action. The U.S. designated cartels as terrorist organizations in early 2025, and kinetic anti-cartel activities have increased throughout Latin America. The potential for geopolitical instability is a lingering risk. If the United States decides to directly engage cartels in Mexico using unmanned systems or troops, it could shift the response by Cartels, which have largely avoided direct interference with key U.S.-related industries or transit routes.

The United States continues to account for the lion's share of FDI into Mexico, with China remaining a very small partner, focused heavily on the automotive sector.

Chinese exports to Mexico have risen significantly in the 2010s and 2020s, in part to take advantage of the growing Mexico market, but more often as inputs to products that will ultimately be sold inside the United States.

Chinese imports from Mexico remain tiny by comparison to the United States or even Canada, providing the Chinese with a significant trade surplus in their Mexican trade balance.